You’ve packed the truck, delivered the goods, and the event went off without a hitch. No damage, happy client. Now comes the part nobody talks about: processing the refund on that security deposit you collected four weeks ago.

For most event rental businesses, that moment is just another task on a list that’s already too long. You collected the deposit, held it, inspected the inventory post-event, confirmed nothing was damaged, and now you have to actually give the money back — all while your team is prepping for three events this weekend. Multiply that by every job on your calendar and you’re spending real time managing money that was never yours to keep.

There’s a better way to protect your business, and it doesn’t involve holding anyone’s money. Non-refundable damage waivers give you the same protection with a fraction of the admin. And your clients actually prefer them.

Key Takeaways:

-

Replace refundable deposits with a non-refundable damage waiver on every job.

A flat, upfront fee — typically around 5% of the order total — collects once and requires no return workflow, saving your team significant admin time across a full season of events.

-

Have an attorney review your waiver language before you start collecting it.

Non-refundable fees are permitted in most states with proper contract disclosure, but the specific language needs to hold up in your jurisdiction to actually protect you.

-

Review the damage waiver terms verbally with every client at signing.

Clients don’t read contracts, and a brief walkthrough before the event sets clear expectations that make post-event conversations much less likely to become disputes.

-

Document inventory with photos at departure and return, and attach them to the event record in your software.

That photo trail is your factual defense if any question about responsibility ever comes up, and keeping it organized by job makes it easy to find.

-

For high-value events, consider requiring client-purchased event insurance alongside the waiver.

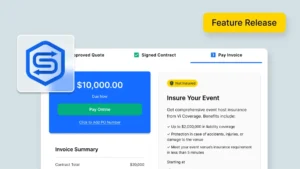

The waiver handles everyday incidents; insurance covers theft, gross negligence, and major losses — and Goodshuffle Pro’s Event Insurance integration lets clients buy it right at checkout with no extra friction.

Why So Many Rental Businesses Are Still Using Security Deposits

Security deposits feel like common sense. Something could get damaged, so you hold money as collateral. If everything comes back clean, you return it. If something gets trashed, you keep it. Simple enough.

The problem is that this model was designed for landlords, not event rental companies doing dozens of jobs a month. A landlord holds one deposit per tenant for months or years. You’re potentially collecting, holding, and returning deposits on every single job you run. That’s a completely different operational reality, and the traditional deposit model doesn’t account for it.

Most rental businesses start with deposits because that’s what they’ve seen other businesses do, or because it feels like the most protective option. And it is protective… in theory. But protection on paper doesn’t mean much if the actual process of enforcing it is eating up your admin hours and creating friction with clients every time something minor happens.

There’s also the reporting problem. When refundable deposits flow in and out of your accounts, your financial picture gets blurry. Are you looking at actual revenue, or deposits waiting to go back? For businesses that are trying to get a clear read on cash flow, especially during busy season, that ambiguity is a real headache.

The Hidden Cost of the Refundable Deposit Cycle

Here’s the thing about a refundable deposit: every single one is a multi-step process with multiple failure points. You collect it. You hold it somewhere — ideally in a tracked account, but realistically in whatever system you have. You do a post-event inspection. You make a damage determination. Then you either initiate a refund or justify keeping it. And if the client disagrees with your assessment? Now you’re in a negotiation.

That last part is where things get expensive, and not just in terms of time.

Deposit disputes are one of the most common sources of tension in the rental industry. The moment you tell a client you’re keeping their deposit — even partially, even for legitimate damage — you’ve opened a conversation that often turns adversarial. They dispute the damage. You pull up your inspection notes. Someone ends up unhappy. In the worst cases, a disputed deposit becomes a chargeback, which costs you fees, time, and potentially the payment itself.

Even when there’s no dispute, you’re still doing the work. Say you run 200 events per year and charge a $300 refundable deposit on each. If even half of those require a straightforward refund with no drama, that’s 100 refund transactions — each one requiring someone on your team to initiate, confirm, and record. At 10 minutes per transaction, that’s over 16 hours of admin time annually, just on refunds that were never in question.

The emotional cost matters too. Clients who’ve paid a deposit spend the tail end of your relationship waiting to see if they get their money back. That’s not a great headspace for a client you want to re-book next year. Even happy clients sometimes forget they paid a deposit, then remember it at an inconvenient time and reach out wondering where their $300 is. Every one of those check-ins is a small interruption, but they add up.

How Non-Refundable Damage Waivers Change the Math

A non-refundable damage waiver converts all of that back-and-forth into a single transaction. The client pays it as part of their invoice. It’s disclosed clearly at signing. And when the event is over, there’s nothing to return, nothing to negotiate, and nothing to track down.

That’s simpler for you, and it’s a better experience for clients too. A small, known, upfront fee is much easier to budget for and accept than the ambiguity of a deposit they might or might not get back. When you frame it right — “a 5% waiver so we don’t have to hold a large deposit from you” — most clients hear that as a benefit, not a cost.

On your end, the operational simplicity is real. No return workflow means no refund processing, no accounts receivable complexity, and no questions about where that payment went three weeks later.

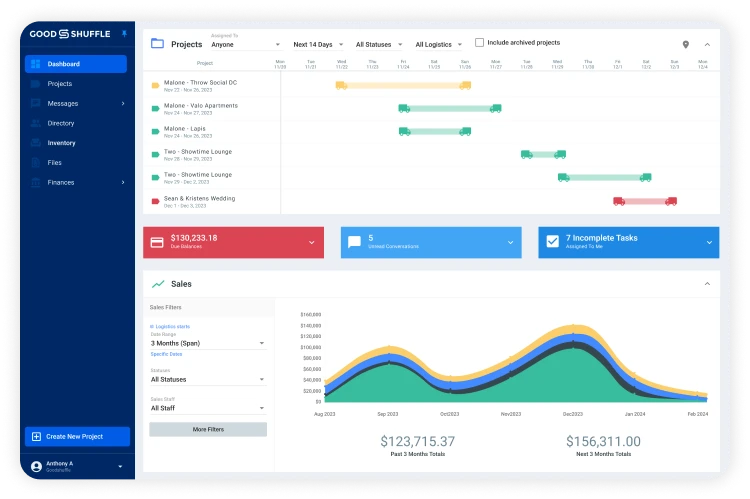

Goodshuffle Pro tracks all payments on a project, so your team sees exactly what’s been collected and what’s confirmed revenue (no guessing about whether a line item is a deposit or an actual payment). That clarity matters when you’re reviewing reports at the end of the month or trying to forecast for a busy season.

Minor damage scenarios get handled automatically, too. A scuffed chair leg, a broken glass, a piece of décor that came back with a crack — instead of invoicing the client after the fact and having a conversation about whether the damage really warrants a charge, the waiver absorbs it. You’ve already been paid. No awkward call required.

For major damage — genuine negligence, theft, significant loss — the waiver doesn’t limit you. Your contract still gives you the right to charge beyond the waiver amount, and you still have the client’s card on file through Stripe to do it. The waiver covers the everyday stuff so you’re not constantly having small, annoying conversations. It doesn’t prevent you from having the big, necessary ones.

Setting Up Your Damage Waiver the Right Way

The most important first step is getting an attorney involved. Non-refundable fees are permitted in most states, but local laws vary, and the language in your contract needs to be airtight. A well-written damage waiver that’s been reviewed by a lawyer creates enforceable expectations before the event — when emotions are lower and clarity is higher.

Beyond the legal piece, there are a few things that make a damage waiver actually work in practice.

Be specific about what the waiver covers and what it doesn’t. Clients should understand that normal wear and tear is their responsibility to a point, that the waiver handles minor accidental damage, and that major damage or negligence isn’t absorbed by a flat fee. Don’t leave room for debate about where the line is. If stemware is covered, say so. If damage from negligence is not, say that too.

Review the contract verbally with clients before they sign. People don’t read contracts. Going through the key terms out loud accomplishes two things: it ensures your client actually understands what they’re agreeing to, and it gives you a chance to spot any red flags before you’ve loaded the truck. A client who gets combative or defensive during a straightforward contract review is telling you something worth paying attention to.

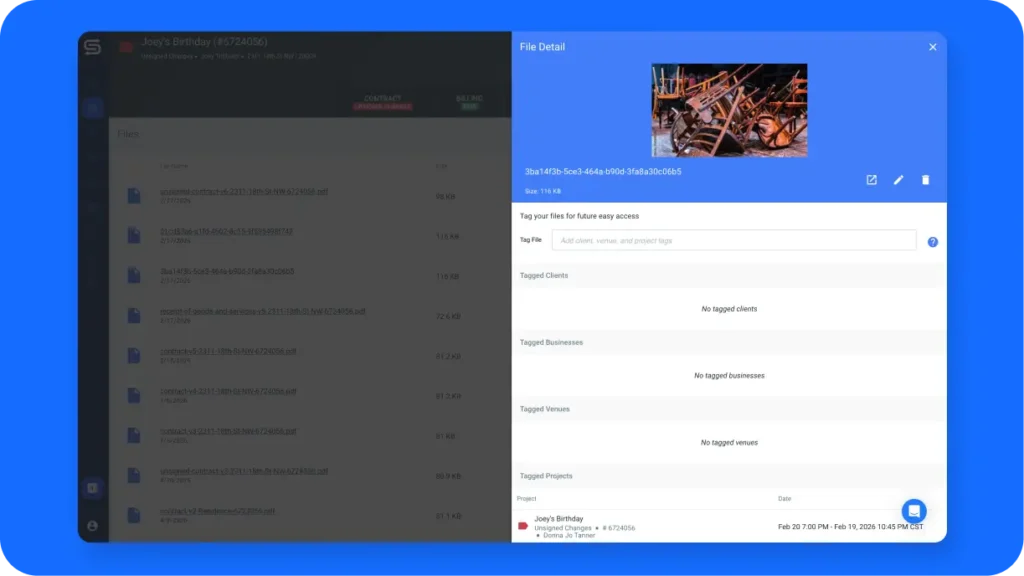

Document your inventory on the way out and the way back in. Photos before items leave your warehouse and after they return give you a factual record if anything is ever questioned. Your team can upload those photos directly to the event’s project in Goodshuffle Pro, so everything is attached to the right job. No hunting through phone cameras or shared drives six weeks after the fact. That documentation protects you and your client both.

When Client-Purchased Event Insurance Makes Sense

A non-refundable damage waiver is a strong foundation. For some jobs, it’s all you need. But for larger events, high-value inventory, or clients who want more comprehensive protection, there’s a step up worth knowing about: having the client purchase event insurance directly.

The waiver is a flat fee you set based on your judgment of risk. Event insurance scales automatically with the complexity and size of the event — more coverage where there’s more exposure, without you having to recalculate anything. And because it’s the client’s policy, the financial responsibility stays entirely with them. If something goes wrong, their insurance handles the claim. You’re not negotiating with anyone.

There’s also the coverage scope to consider. A damage waiver handles everyday accidents. Event insurance can cover theft, gross negligence, third-party liability, and scenarios a flat fee simply can’t address. For a large corporate event or a wedding with high-ticket rentals, a 5% waiver might be appropriate for routine incidents, but it doesn’t protect you from the truly catastrophic situations.

Goodshuffle Pro has an Event Insurance integration built directly into the checkout flow. Clients can purchase coverage without leaving the quoting process — no external forms, no separate links, no back-and-forth. You can even require insurance for certain event types, which removes the decision from your client’s hands and protects your business automatically.

For the right jobs, that combination of a non-refundable damage waiver and required client-purchased insurance is about as protected as an event rental business can get.

FAQs

A security deposit is a refundable amount held until after the event, which you then return if no damage occurs. A non-refundable damage waiver is a smaller, upfront fee — typically around 5% of the order — that covers minor damage automatically, with no return workflow required on your end.

In most states, yes — but local laws vary. You’ll want an attorney to review your contract language and confirm what’s permissible in your jurisdiction before putting a damage waiver in place. Proper disclosure in the signed contract is typically required.

The waiver handles everyday incidents — scuffs, a broken piece of stemware, minor wear beyond normal use. For major damage or gross negligence, you still have your contract, the credit card on file, and the right to charge beyond the waiver amount. The waiver doesn’t cap your recourse; it just takes care of the routine stuff automatically.

Frame it as a convenience for them, not just a protection for you. Something like: “We charge a small non-refundable damage waiver — about 5% of your order — so you’re covered for accidental incidents and we don’t have to hold a large deposit from you.” Most clients prefer the clarity of a known, upfront cost over the ambiguity of a deposit they might or might not get back.

For larger events or high-ticket inventory, yes. A damage waiver covers everyday incidents; event insurance covers the truly catastrophic stuff — theft, gross negligence, third-party liability. Goodshuffle Pro has an Event Insurance integration that lets clients purchase coverage directly at checkout, which removes the admin burden from your team entirely.

Share On